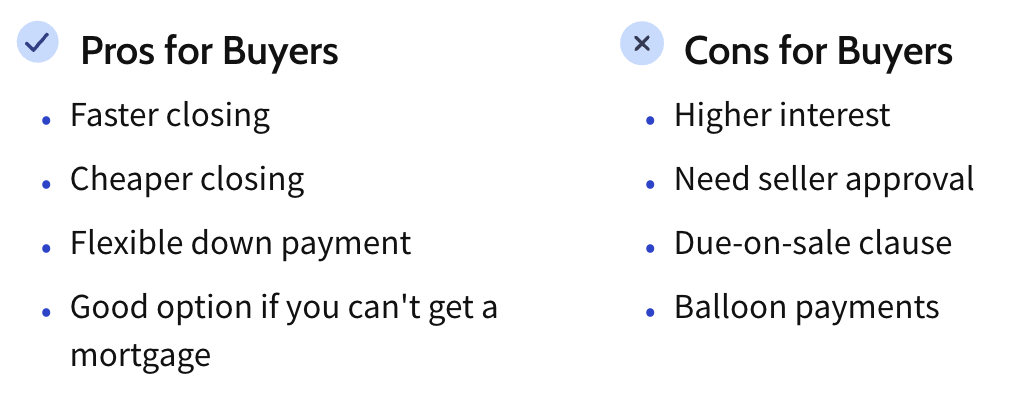

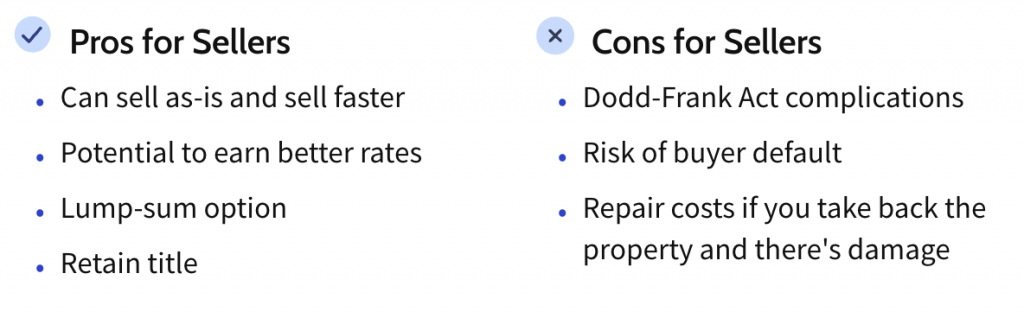

While it’s not common, seller financing can be a good option for buyers and sellers under the right circumstances. Still, there are risks for both parties that should be weighed before signing any contracts.

If you’re considering owner financing, it’s generally in your best interest to work with a real estate attorney who can represent you during negotiations and review the contract to make sure your rights are protected.

Source: Investopedia Click here for article